|

POPULAR ARTICLES

- e-Invoicing in France 2026: Timeline, Requirements, Guidelines & Format

- What is a PDP, OD and PPF in France e-Invoicing?

- All About e-Reporting under France e-Invoicing

- VAT in France 2026: Rates, Registration, Filing, Payments & Penalties

- France e-Invoicing and e-Reporting FAQs: Rules, Scope & 2026 Requirements

- Credit Note in France: Meaning, Usage, Example & Template

- Factur-X in France: What It Is, How It Works and Steps to Generate

- SIREN and SIRET Numbers: How to Apply and Where to Get Them

- Common e-Invoicing Mistakes in France & How to Avoid Them

- XML vs PDF/A-3 in e-Invoicing: Handling Structured & Unstructured Data

- Top 7 Misconceptions About E-Invoicing in France for 2026

- What is the EN 16931 Electronic Invoicing Standard in France?

- Handling Structured & Unstructured Data in e-Invoicing: XML and PDF/A-3 Explained

YOU MIGHT BE INTERESTED IN

e-Invoicing France 2026: Timeline, Requirements, Guidelines & Format

e-Invoicing France rolls out from September 1, 2026. In France, structured e‑invoice formats are mandatory for all VAT‑registered businesses. As part of this legislation, companies are required to exchange invoices electronically through certified systems rather than using traditional paper or PDF invoices.

Key Takeaways

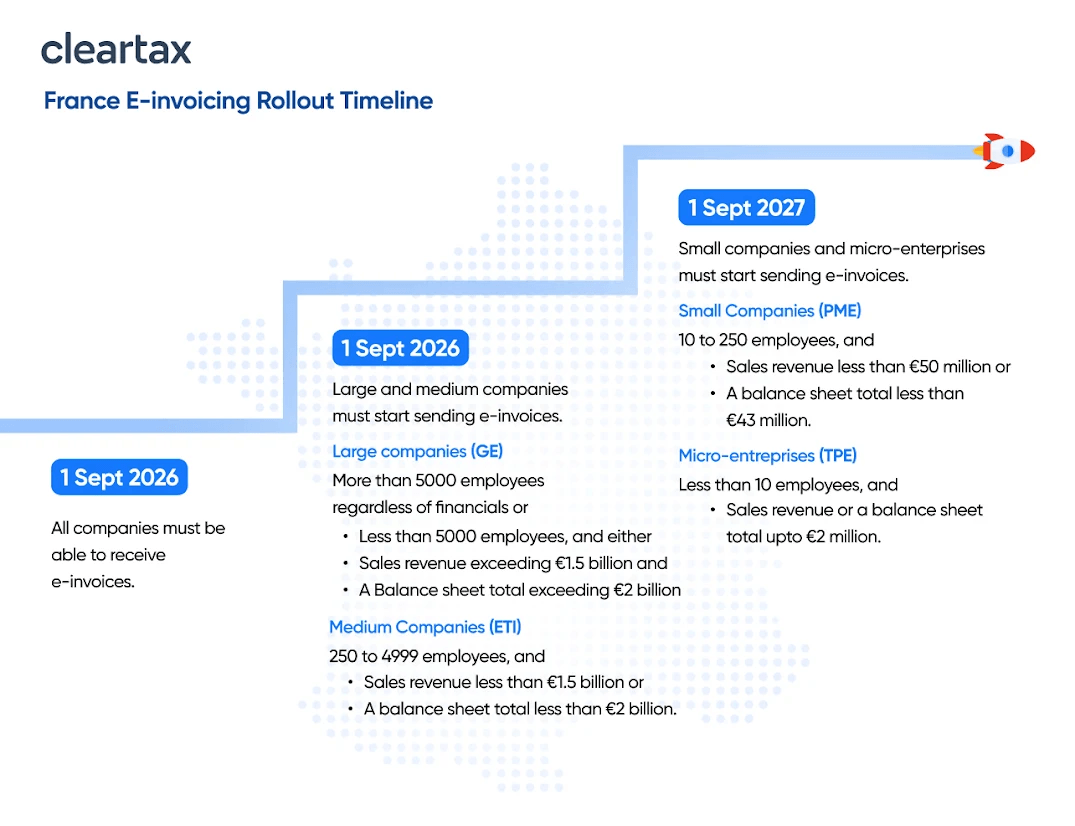

- From 1st September 2026, large and medium enterprises need to issue e-invoices. Small and micro-enterprises should start from 1st September 2027 onwards.

- The invoice should be in an accepted format, such as Factur-X, UBL, or CII. Transactions should be conducted through certified Approved Platforms (PAs).

- For B2B transactions, only structured electronic invoices are permitted. Traditional paper and standard PDF invoices are not accepted.

- E-reporting is mandatory for B2C, cross-border, and other non-B2B transactions.

What is e-Invoicing in France?

e-Invoicing in France is the process by which companies must issue, transmit, and receive invoices in electronic format, in accordance with the digital standards and platforms prescribed by law. This way, the information from the invoices can be automatically processed and reported to the French tax authorities.

Several laws have been enacted to ensure there is a legal framework for France’s compulsory use of electronic invoices.

- Article 153 of the Finance Law in 2020.

- The legal provision was translated into reality through Article 26 of the Finance Law n° 2022-1157 of 16 August 2022.

- The implementation of the provisions was amended in Article 91 of the Finance Law of 2024, whereas Article 123 of the Loi de Finances pour 2026 (adopted 2 February 2026, promulgated 19 February 2026) has made the latest amendments.

In France, all companies with VAT obligations are subject to B2B e-invoicing.

France e-Invoicing Timeline and Compliance Deadlines

The original scheduled timeline of July 1, 2024, for the implementation of electronic invoicing was postponed. This gives everyone sufficient time to be prepared for this major change. New details on the implementation date and the prerequisites have been clearly set out in the latest Finance Law.

What is e-Reporting in France?

e-Reporting in France refers to the electronic transmission of specific transactional and payment data to the French tax authorities for certain operations that are not covered by the mandatory B2B e-invoicing regime.

Who Must Perform e-Reporting?

- French Businesses: Every business incorporated in France should electronically report those transactions that fall outside the scope of the e-invoicing obligation.

- Foreign Businesses: Any business registered for VAT in France but that does not have a permanent establishment in France should also report electronically.

Who must comply with e-Reporting Obligations?

As per the French tax administration, the transactions that should be reported electronically are:

- Business to Consumer (B2C): The sales of goods/services by businesses in France to consumers (not applicable for B2B electronic invoicing).

- Exports: The supplies of goods/services from France to countries which are not part of the European Union.

- Imports: The purchases of goods/services by businesses in France from countries which are not part of the European Union.

- Intra-community EU Exports: The exportation of goods and services from France to other EU member countries.

- Intra-community EU Imports: The importation of goods and services into France from other EU member countries.

How is e-Reporting Performed?

The procedure for e-reporting is undertaken via approved platforms (PA) or solutions compatible (SC), which are the new terms for dematerialising operators (OD), and which transmit the information to the tax authority. The information will include pertinent information relating to the invoice, amount, VAT, and payments, among others, depending upon the nature of the transaction.

E-reporting must be completed within the deadlines set by the French tax department.

e-Invoicing vs e-Reporting: What’s the Difference?

e-Invoicing replaces traditional B2B invoicing with real-time structured invoice exchange, while e-reporting provides tax authority visibility into transactions outside the e-invoicing scope.

Here are the major differences

Aspect | E-Invoicing | E-Reporting |

Scope | Domestic B2B transactions (both parties VAT-registered in France) | Transactions outside e-invoicing scope: B2C, cross-border B2B, exports |

Transaction Types | Business-to-business sales between French entities | B2C sales, international B2B (EU & non-EU), exports |

Invoice Format | Mandatory structured formats: UBL 2.1, UN/CEFACT CII, or Factur-X | Any format for customer invoice; structured data to tax authority |

Data Detail Level | Complete invoice detail: all line items, full party info, VAT breakdown | Summary/aggregate data only (daily totals for B2C by SIREN) |

Recipients | Buyer + French tax authority (dual transmission) | French tax authority only (single transmission) |

Submission Timing | Real-time/immediate upon invoice creation | Periodic: every 10 days for transactions, monthly for payments |

Lifecycle Tracking | Yes - tracks sent, received, rejected, accepted, paid, collected | No - no status tracking required |

Primary Purpose | Replace traditional invoicing; enable automated VAT reporting | Provide tax authority visibility into non-e-invoiced transactions |

Platform Use | Mandatory use of certified Approved Platforms (PA) | Via Approved Platforms or PPF; more flexible than e-invoicing |

Implementation Date | September 1, 2026 (large/medium); Sept 1, 2027 (small/micro) | September 1, 2026 (large/medium); Sept 1, 2027 (small/micro) |

Why is e-invoicing being introduced in France?

The French Government is committed to the implementation of e-invoicing for businesses. This reform aims to:

- Enhance their competitiveness by reducing administrative burden and increasing productivity through dematerialisation.

- Simplify reporting obligations by automating VAT declarations.

- To avoid fraud cases and favour the legitimate businesses

- Improve real-time visibility into business operations.

French e-Invoicing Model and Framework

The French government has opted for a more advanced 5-corner model for electronic invoicing and reporting to minimise VAT fraud and facilitate e-invoicing and e-reporting to tax authorities.

Y-Model to 5-Corner Model: Structure & Major Components

In its early stage, France envisioned a hybrid solution ("Y-model"), under which enterprises would be able to send invoices through the public portal (PPF), approved platforms (PAs), or dematerialisation operators (ODs). At that time, the PPF was of great importance in the structure of this scheme.

As of the end of 2024, France announced a move to a strict 5-corner model, under which all e-invoices must be sent exclusively through certified PAs, which should handle both invoice transfer and e-reporting to the tax administration. This model will come into effect from September 2026. Now, the function of the PPF is limited to that of the Annuaire Central (Central Directory) and Concentrateur de Données (Data Concentrator).

Authorised Formats

According to the DGFiP, there are three key structured formats:

- Factur-X (combined PDF/A-3 and XML format)

- UBL 2.1 (Universal Business Language)

- UN/CEFACT CII (Cross Industry Invoice)

Note: The Peppol BIS Billing 3.0 is a profile of UBL 2.1 and is not a separate authorised format. EDIFACT does not fall within the authorised formats under the French mandate and should be converted to one of the aforementioned three formats via the PA’s certification process.

Additionally, France gained status as a Peppol Authority on 8 July 2025.

Key Participants in French e-Invoicing

In France, the e-invoicing system involves various stakeholders who play specific roles in the creation, transmission, receipt, and reporting of invoices. Some of the stakeholders include buyers, sellers, financial institutions, tax agencies, and other institutions. The involvement of these stakeholders makes it easier for businesses to report their VATs.

Participant | Role and Function |

Supplier (Seller) | Creates invoices in approved electronic formats and initiates the invoicing process via a certified PDP. |

Buyer (Customer) | Receives invoices through their chosen PDP, processes, pays, and manages any disputes or corrections. |

PDP (Partner Dematerialization Platform) | Validates invoice format, ensures compliance, converts formats if needed, routes invoices, and reports data to the PPF. |

PPF (Public Invoicing Platform) | Maintains the central directory, aggregates invoice and reporting data, and forwards information to the tax authority. |

Oversees the e-invoicing mandate, monitors compliance, and uses data for VAT control and enforcement. | |

OD (Dematerialization Operator) | Assists with format conversion and e-reporting for transmission but doesn’t transmit it themselves |

e-Invoicing Process in France

The French e-invoicing model is efficient, secure, and transparent, as all B2B invoices are transmitted in a standard format via certified platforms.

Invoice: The supplier creates the invoice in one of the three invoice formats recognised as structured invoices (Factur-X, UBL, or CII). In case the supplier is unable to create the invoice in one of the three invoice formats, then the invoice can be changed to the required format by the certified Approved Platform (PA) or the dematerialisation operator (OD).

Sending Invoice via PA: The supplier sends the electronic invoice to a certified PA.

Interoperability and Delivery: If the invoice recipient has a different PA than the supplier, the supplier’s PA will deliver the invoice to the recipient’s PA.

E-Reporting: The PA gathers the required invoice data and, if necessary, payment status data, and transfers it to the PPF for tax reporting. For transactions that fall outside e-invoicing (B2C or international), PAs or ODs will handle e-reporting to the PPF.

Processing by the Tax Authority: All collected data is transferred to the French tax authority (DGFIP) for compliance checks and VAT control.

What are the Requirements for e-Invoicing in France?

In order to comply with the e-invoicing and reporting regulations of France, the following are some of the requirements that the organisations have to adhere to:

- Electronic Format: The invoices should be prepared using a recognised electronic format such as Factur-X, UBL, or CII.

- Certified Platforms: All invoices should be transmitted and received through government-certified electronic invoicing platforms, referred to as Approved Platforms (PAs).

- Real-time Reporting: Invoice information will be automatically transmitted to the French tax authority.

- Electronic Reporting for Other Transactions: In cases where electronic invoicing does not apply to certain transactions (e.g., sales to consumers or cross-border transactions), important information about these transactions must still be reported electronically.

No More Basic PDF or Paper Forms: Regular paper invoices or PDFs sent by email can no longer be used unless they are converted to an approved electronic format.

How Should Businesses Prepare for France e-Invoice Mandate

For companies to transition successfully into France's e-invoicing mandates, the following strategies should be implemented:

1. Formation of an internal task force: The internal task force should comprise managers, accountants, and IT staff who will oversee the transition process.

2. Audit of current processes: This step involves auditing the current invoice generation, accounting, and ERP systems to see what processes have already been digitised and those that require improvement.

3. Assessment of technical capability: It is imperative for companies to evaluate their current systems to check whether they can generate invoices in the required format (Factur-X, UBL, and CII).

4. Select a Certified PA: Conduct research to identify a certified PA. This PA will manage the transmission, processing, and reporting of your invoices.

5. Training and Communication: Train all employees who are going to be involved in the process of implementing the new e-invoice management system on the new procedures and regulations. Ensure they understand how to utilise the new PA.

6. Testing and Integration: Test the system and resolve any issues with formatting, transmission, or reporting before full implementation.

What are the benefits of e-invoicing in France?

Here are a few benefits of e-invoicing in France:

- Increased productivity due to faster processing times

- Optimised cash flow with shorter payment times

- Increased visibility of all processes & performance

- Lowered operating costs

- Easy preparation of VAT returns

- Reduced VAT frauds

Penalties for non-compliance with France e-invoicing

Below are the penalties that take into account the amounts set officially in Article 123 of Loi de Finances pour 2026 (Law n° 2026-103 of 19 February 2026), thus replacing the former system of penalties. There are different penalties imposed for violations of either the e-invoicing or e-reporting rules.

Non-Compliance Type | Penalty per Instance | Maximum Penalty (per year) |

Failure to issue an e-invoice | €50 per invoice | €15,000 (per business) |

Failure to transmit e-reporting data | €500 per transmission | € 15,000 (per business per calendar year ) |

Failure by PA to transmit/receive invoice | €50 per invoice | €45,000 (per PA) |

Failure by PA to transmit e-reporting data | €750 per failed transmission | €100,000 (per PA) |

Missing or inaccurate invoice information | €15 per error (capped at 25% of invoice value) | - |

Persistent non-compliance (no accredited PA used) | €500 fine applies first, followed by a new 3-month notice. Thereafter, €1,000 fine, recurring quarterly penalty. | - |

Additional Notes:

- Penalties will be levied separately for violations of electronic invoices and reports.

- The penalty for failure to provide correct invoice data shall not exceed 25% of the total amount of the invoice.

- Fraudulent invoicing carries a heavy penalty due to its importance in tax evasion.

- Penalties are cumulative and may be levied alongside other fines.

- The annual limit on penalties imposed on PAs is higher than that for others, given their importance.

- On 7 May 2026 (annual E-Invoicing Day), the Director General of DGFiP, Amélie Verdier, stated that no penalties will be imposed from 1 September 2026, as there will first be contact with businesses before any enforcement can occur.

How ClearTax Can Help with e-Invoicing Implementation in France

ClearTax is now an Approved Platform (PA) for France e-invoicing and e-reporting, recognised under the French tax administration’s accreditation framework providing legal authority to help businesses issue, receive, validate, route, and report compliant electronic invoices under France’s 2026 mandate.

- Connect effortlessly with any ERP or POS system via APIs.

- Compliant e-invoice exchange with the French Public Portal (PPF).

- Manage e-invoicing and compliance from a single secure dashboard.

- Automatic updates to stay compliant with French regulations.

- 99.99% uptime for uninterrupted invoicing.

- Advanced validation for faster, error-free processing.

- Instant alerts for invoice status changes.

- Automated updates to improve vendor and customer interactions.

Invoice Lifecycle Status Management in France

The e-invoicing initiative implemented by the French government is based on a mandatory real-time status tracking of all invoices, which changes their status from static objects to dynamic ones. Using standardised statuses from creation to submission, acceptance, rejection, payment, archiving, etc., all transactions become visible to businesses, platforms, and DGFiP.

This scheme consists of 14 potential statuses, with only four being obligatory as per the AFNOR standard XP Z12-012:

- Déposée (Submitted/Deposited)

- Rejetée (Rejected - technical refusal on the platform side)

- Refusée (Refused – commercial refusal from the buyer's side)

- Encaissée (Cashed /Payment Received - confirms that payment has actually been received by the supplier)

Remark: Encaissée confirms that funds have been received by the supplier, while Paiement transmis (Payment Sent) - an optional status - shows that the payment has been initiated or dispatched by the buyer. In practice, a buyer may trigger "Payment Sent" when they release a transfer, but "Encaissée" is only updated once the supplier receives the money. The two statuses can therefore coexist in sequence on the same invoice, and neither replaces the other.

These statuses use automatic, real-time CDAR messaging for transparency, anti-fraud purposes, and VAT compliance. This criterion is an integral part of France’s e-invoicing reform project for B2B transactions, which aims to create a fully digital audit process.

Frequently Asked Questions

About the Author

Rajan Rauniyar

I’m a Senior Content Writer at ClearTax, specializing in e-invoicing, VAT, and Tax compliance. Over the years, I’ve researched and written everything from blog posts to whitepapers and product guides, helping ClearTax expand in Malaysia, KSA, UAE, Singapore, Belgium, France and beyond. My goal is to write the most comprehensive, understandable, readable, and accurate content on any topic that has ever existed on the internet. Read more

Your data security and privacy matter most to us.