E-Invoicing in Germany: Obligations, Timeline, Requirements, Format & Examples

Updated on: Mar 5th, 2026

|

36 min read

Switch Language

Germany has announced mandatory e-invoicing requiring all VAT-registered businesses to issue structured, machine-readable electronic invoices for domestic B2B sales. This reform standardizes invoice formats, enhances tax compliance, and gradually phases out traditional paper and PDF invoices for most business dealings.

Key Takeaways: e-Invoicing Requirements in Germany

- e-invoices must use structured formats like XRechnung or ZUGFeRD 2.1+, enabling automated processing.

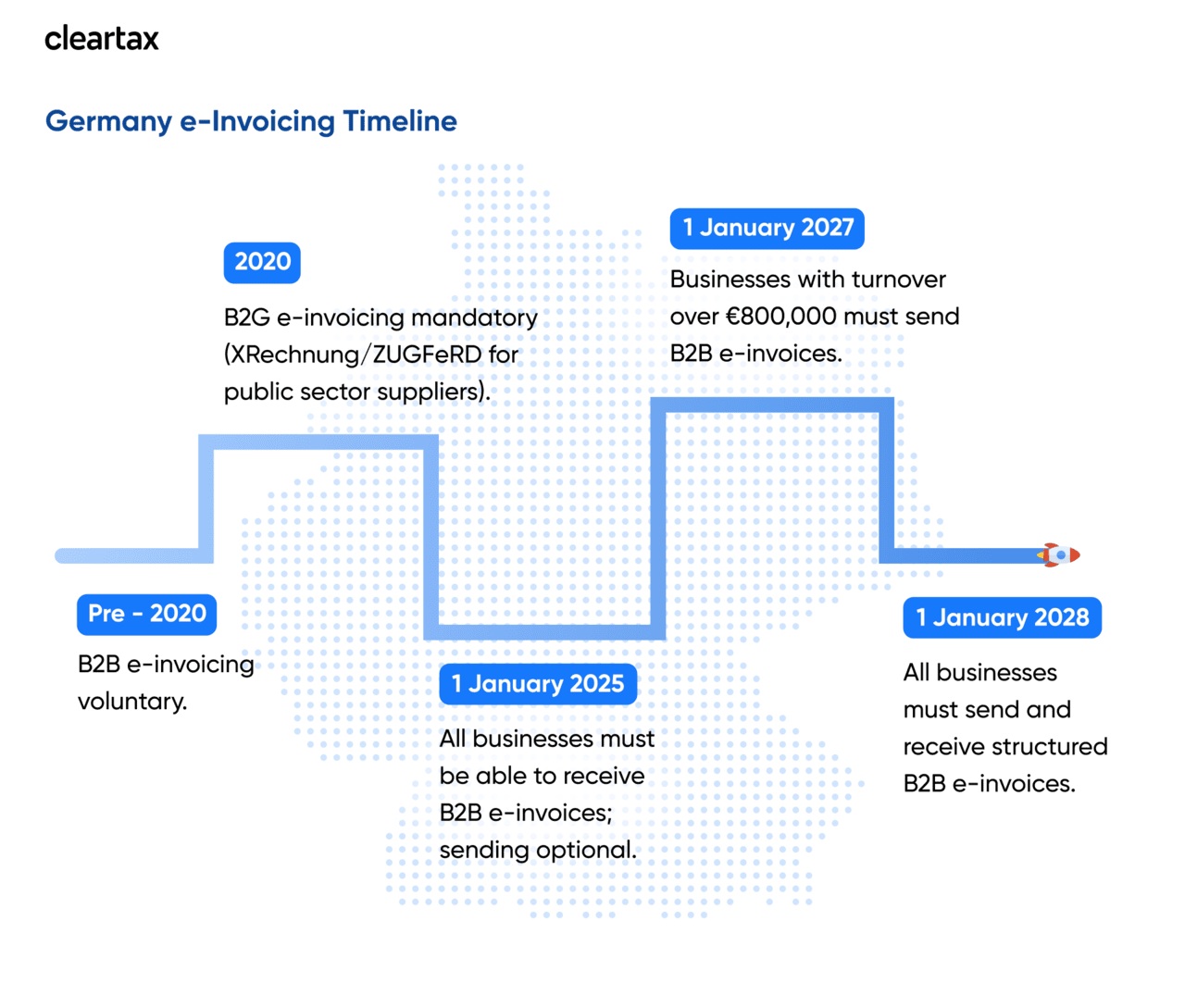

- All businesses must be able to receive e-invoices from 1 January 2025, and issuing becomes mandatory in phases through 2028 (with a specific exemption for small businesses under §19 UStG (annual turnover up to €22,000).

- e-invoices must be securely archived in their original format for at least 10 years.

- Exemptions apply to B2C transactions, invoices under €250, passenger tickets, and VAT-exempt sales, and inter EU transactions

What is e-Invoicing in Germany?

e-Invoicing, or electronic invoicing, is the process of issuing, sending, receiving, and storing invoices in a structured digital format that enables seamless, automated processing by computers without manual data entry or paper handling.

In Germany, e-invoicing means exchanging invoices as structured electronic format (not a normal PDF emailed to a customer). For B2B and B2G use cases, the invoice must be machine-readable and compliant with EN 16931, enabling automated validation and posting in accounting systems.

Germany’s B2B e-invoicing mandate is introduced through the Growth Opportunities Act (Wachstumschancengesetz) (enacted in March 2024) and implemented via updates to Section 14 of the German VAT Act (UStG), The German tax authority also released the official E-Invoicing Guidelines (in German) on 25 October 2025.

Germany E-Invoicing Timeline and Compliance Deadlines

Germany is transitioning from voluntary electronic invoicing to a phased mandatory e-invoicing system for all B2B transactions. While e-invoicing has been required for business-to-government (B2G) invoices since 2020, the focus is now on B2B e-invoicing.

Who must comply with Germany's e-Invoicing mandate?

The following transactions and entities are subject to Germany's e-invoicing mandate:

- All domestic B2B Businesses: For transactions where both the supplier and the recipient are based in Germany.

- Businesses Providing Taxable Supplies under VAT: Any taxable supply of goods or services that fall within the scope of German VAT law (UStG).

- Business-to-Government (B2G) suppliers: Business invoicing to federal and state public administrations.

- Foreign Entities with Local Establishments: Foreign businesses operating in Germany with "fixed establishment" (e.g., a physical office or warehouse)

Who all are exempted from e-invoicing in Germany

The following transactions and entities are exempt from Germany's e-invoicing mandate:

- Small-amount invoices with a gross total of €250 or less.

- Passenger transport tickets, which are exempt from structured invoice requirements.

- VAT-exempt transactions as defined by specific provisions in the VAT Act (UStG)

- Foreign businesses without Local establishment: that are only VAT-registered in Germany, but do not have a fixed establishment, are not subject to this mandate.

- Cross-border transactions whether incoming or outgoing.

- Business-to-consumer (B2C) transactions: Sales to private individuals remain outside the scope. Traditional formats such as paper receipts or PDFs can still be used for consumer sales.

For which type of transactions is e-Invoicing required in Germany

Germany’s B2B e-invoicing mandate mainly depends on where the parties are established and whether the transaction is domestic B2B. Use the tables below to quickly determine what format, VAT treatment, and document wording typically apply.

Supplier | Buyer | e-Invoicing Requirement (Yes/No) | Treatment |

Established in Germany | Established in Germany (business) | Yes | Standard domestic B2B. EN 16931 e-invoice. VAT 19%/7% with totals. |

Established in Germany | Established in Germany (business) | Yes | Reverse charge. EN 16931 e-invoice. Net only, “Reverse charge” note. |

Established in Germany | Established in another EU country (business) | No | Intra-EU B2B. Out of scope. 0% VAT rules, buyer VAT ID. |

Established in another EU country | Established in Germany (business) | No | Out of scope for German mandate. Reverse charge often applies. |

Established outside the EU | Established in Germany (business) | No | Import. Out of scope. Import VAT via customs docs. |

Established in Germany | Established outside the EU | No | Export. Out of scope. Keep export evidence, 0% VAT. |

Small business using the small-business VAT scheme (annual turnover up to €22,000) | Established in Germany (business) | No (issuing exempt) | May issue paper/PDF with small-business VAT note. |

Established in Germany | Small business using the small-business VAT scheme (annual turnover up to €22,000) | Yes (receiving) | Buyer must receive e-invoices. Supplier follows mandate phase-in. |

Established in Germany | Private consumer (B2C) | No | B2C. Out of scope. |

Established in Germany | Buyer status unclear | Depends | Treat as B2B if entrepreneur; otherwise B2C. Document status. |

E-Invoicing Formats in Germany: XRechnung & ZUGFeRD

EN 16931-compliant formats like XRechnung and ZUGFeRD are the officially accepted electronic invoice formats for public sector transactions and form the basis for the phased B2B e-invoicing mandate. Both formats defines the mandatory data structure and content required for electronic invoices in Germany.

1. XRechnung (XML)

Germany’s official EN 16931 implementation, used widely for B2G and accepted for B2B. It’s designed for system-to-system processing, so finance teams typically view it through ERP/accounting tools rather than “reading” the file directly.

2. ZUGFeRD (Hybrid PDF/A-3 + Embedded XML)

A practical hybrid for finance teams: a readable PDF plus structured XML for automation. For compliance, only the EN 16931-aligned profiles (2.0.1+ / COMFORT or EXTENDED) should be treated as mandate-ready, and the XML is the legally relevant part.

3. EDIFACT / Legacy EDI

Legacy EDI setups can continue during the transition where already established and agreed by both parties. Long-term, the requirement is that the EDI flow must be able to produce/extract EN 16931-compliant structured data (especially relevant from 2028).

4. Peppol BIS Billing 3.0 (UBL)

A standardized way to exchange structured invoices via the Peppol network. It’s a strong option when you need interoperability across many trading partners, provided the content remains correctly mapped to EN 16931.

5. XML (General)

“XML” alone is not a compliance indicator. What matters is whether the file follows an accepted EN 16931 implementation (e.g., XRechnung XML, ZUGFeRD embedded XML, or EN 16931-mapped UBL).

Validity and Lifespan Comparison of e-Invoicing Formats in Germany

Format | What It Is | EN 16931 Compliant? | Valid for Mandatory B2B? | Use Window (Practical Timeline) |

XRechnung | Pure XML | Yes | Yes | Valid since 2025; recommended for structured B2B; mandatory-ready for 2028+ |

ZUGFeRD 2.0.1+ (EN 16931 profile) | PDF + embedded XML | Yes (specific profiles only) | Yes | Valid since 2025; mandatory-ready for 2028+; XML is legally relevant |

Peppol BIS Billing 3.0 (UBL) | Structured UBL via Peppol | Yes (if mapped correctly) | Yes (if EN 16931-compliant) | Valid since 2025; mandatory-ready for 2028+ if mapping stays EN 16931-compliant |

EDIFACT / legacy EDI | EDI messages | Not necessarily | Not by default | Transition use 2025–2027 (by agreement); from 2028 must output EN 16931 |

PDF (non-hybrid) / Paper | Visual document only | No | No | Only for exceptions / transitional cases; not valid for in-scope mandatory B2B |

Mandatory Data Fields Required in a Germany-Compliant e-Invoice

Here's the list of Mandatory Data Fields Required for e-Invoicing in Germany based on EN 16931 Standard:

- Invoice Identification

- Seller Details

- Buyer Details

- Line-Item Detail

- VAT Information

- Totals and Payables

Know more about Mandatory Data Fields Required for an e-Invoice in Germany

E-Invoicing Framework in Germany

Germany’s e-invoicing framework is built to enable flexible, secure, and interoperable electronic invoice exchanges across both the private and public sectors.

- Decentralized Exchange: Unlike some countries, Germany does not require B2B invoices to pass through a central government portal (clearance model). Instead, invoices are exchanged directly between businesses, using email, EDI (Electronic Data Interchange), or networks like Peppol.

- Public Sector (B2G) Portals: For invoicing public entities, suppliers must use official portals such as the E-Rechnungsportal Bund or OZG-RE at the federal level, or state-specific platforms. These are Peppol-enabled and accept XRechnung and compatible ZUGFeRD files.

- Post-Audit Model: Germany uses a post-audit model for e-invoicing, meaning tax authorities may request invoices for audit after the fact but do not automatically receive all invoices in real time.

E-Invoice Transmission Model in Germany

- Email (structured XML or hybrid file attachment)

- EDI networks (subject to transition rules)

- Peppol network

- Direct ERP/API integrations

- Customer/supplier portals (must allow downloading the structured file)

E-Invoicing Process in Germany

Electronic invoice exchange in Germany relies on structured data, compliance with legal standards, and digital automation.

- Invoice Generation: Businesses create e-invoices using ERP, accounting software, or an e-invoicing solution provider. These providers ensure invoices are formatted as XRechnung (XML) or ZUGFeRD (PDF/A-3 + XML) and contain all required data for VAT compliance.

- Transmission: Invoices are sent directly to trading partners via email, EDI, Peppol network, or service provider platforms. The exchange channel is chosen by agreement, but the invoice must remain in a structured format.

- Receipt and Validation: The recipient’s software or e-invoicing provider validates the invoice for format and data integrity. Valid e-invoices are automatically processed into ERP or accounting systems.

- Archiving: All e-invoices must be archived in their original electronic format for 10 years, ensuring authenticity, integrity, and legal audit-readiness.

Note: Invoices to government bodies are submitted through official portals (E-Rechnungsportal Bund, OZG-RE, or state platforms). E-invoicing solution providers can automate submission, integrate with these portals, and validate file compliance.

E-Invoice Archiving and Retention in Germany (GoBD)

Germany requires e-invoices to be archived under GoBD rules in their original electronic format.

- Keep the Original File: XML must remain XML. ZUGFeRD must remain the hybrid file (PDF/A-3 with embedded XML).

- Maintain Integrity and Authenticity: No silent edits. Any corrections must be traceable and logged.

- Apply the Hybrid Invoice Rule: If the PDF and XML differ, the XML is the legally relevant record. The PDF is only a visual rendering.

- Ensure Audit Readiness: Invoices must remain readable, searchable, and exportable during audits.

Retention is generally 8 years, but certain cases still require 10 years depending on tax obligations.

How Businesses Should Transition to E-Invoicing in Germany: Step by Step Guide

Transitioning to e-invoicing is now a strategic necessity in Germany due to new legal mandates and the need for digital efficiency. Companies must ensure compliance while improving invoice accuracy, speed, and traceability.

Step 1: Map Current Invoice Flows:

Document how invoices are created, approved, sent, received, and archived. Identify gaps in digitalization and pinpoint manual bottlenecks.

Step 2: Understand Compliance Requirements

Review which transactions require e-invoicing (B2B, B2G), applicable formats (XRechnung, ZUGFeRD), and upcoming deadlines based on company size and turnover.

Step 3: Upgrade IT Infrastructure

Ensure your ERP or accounting software supports structured e-invoice formats. Evaluate whether existing systems require integration modules or a switch to more advanced platforms.

Step 4: Select the Right E-Invoicing Provider

Compare features, compliance coverage, integration options, and user support among solution providers. Look for certified Peppol access and automatic format validation.

Step 5: Establish Internal Policies

Develop standard operating procedures for issuing, receiving, and archiving e-invoices. Define roles, responsibilities, and escalation paths for invoice exceptions or errors.

Step 6: Train Employees and Communicate Externally

Provide targeted training for accounting, IT, and operations staff. Inform business partners of your new e-invoicing capabilities and preferred exchange channels.

Step 7: Test Thoroughly Before Going Live

Pilot e-invoicing with selected suppliers and customers to ensure interoperability, error handling, and seamless workflow integration.

Step 8: Monitor Regulatory Changes

Regularly review government updates and solution provider communications to stay ahead of evolving legal and technical requirements.

How Germany’s e-Invoicing Differs

Germany’s e-invoicing approach contrasts with other European countries like Poland and France e-Invoicing mandate, especially in terms of centralization, clearance requirements, and transmission models. The following table outlines the main differences:

Feature | Germany | France | Poland |

Model | Decentralized, post-audit | Centralized clearance (real-time to govt) | Centralized clearance (real-time to govt) |

Format | XRechnung (XML), ZUGFeRD (PDF/XML) | Factur-X (EN 16931, PDF/XML hybrid), XML | KSeF XML (custom Polish format) |

Transmission | Direct, Peppol, or public sector portal | All invoices routed via Chorus Pro (central portal) | All invoices routed via KSeF (central platform) |

Human-readable | PDF option via ZUGFeRD | PDF/XML hybrid (Factur-X) | XML only; human-readable optional |

Mandate Timeline | B2G: 2020; B2B: 2025–2028 phased | B2G: 2020; B2B: 2026 (phased) | B2B: 2024 (full clearance from July 2024) |

Tax Authority Access | Audit on request | Real-time, automatic copy to tax authority | Real-time, automatic copy to tax authority |

ClearTax E-Invoicing Solution

ClearTax helps you go live with Germany-compliant e-invoicing faster, with fewer manual touchpoints.

- ERP-Ready Integrations: Connect with SAP, Oracle, Dynamics, and more for automated mapping, validation, and compliant output.

- One Central Portal: Generate, send, track, and archive e-invoices securely from a single dashboard.

- Peppol-Enabled Exchange: Support compliant transmission for Germany and EU public-sector workflows.

- Always Compliant, Audit-Ready: Built-in validations, regulatory updates, and long-term secure archiving.

- Scales With Your Business: Multi-entity support, strong security controls, and guided onboarding.

Conclusion

The e-Invocing mandate in Germany applies strictly to B2B transactions where both parties are established in Germany. Public sector entities already require e-invoices since 2020, submitted through official portals like the E-Rechnungsportal Bund or state systems.

Unlike countries with centralized clearance models, Germany follows a decentralized, post-audit approach: invoices are exchanged directly between businesses without real-time tax authority validation.

This model prioritizes interoperability and flexibility while laying the foundation for potential future EU-wide real-time reporting under the VAT in the Digital Age initiative.

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

Your data security and privacy matter most to us.