|

POPULAR ARTICLES

- E-Invoicing in Germany 2027: Obligations, Timeline, Format & Examples

- How to Receive E‑Invoices in Germany? Format, Process, Validation and Archiving

- E-Invoicing for Small Businesses in Germany: Creating, Receiving, Deadlines & Formats

- Germany E-Invoicing FAQs: Everything You Need to Know German e-Invoicing Mandate

- Mandatory Data Fields Required for an e-Invoice in Germany

- OZG-RE Portal: Features, Registration & Best Practices

- XRechnung e-Invoicing Format? How to Create, Examples, Specifications

- How to Create e-Invoice in Germany: XRechnung & ZUGFeRD Format

- What is EN 16931? Electronic Invoicing Standard in Germany

- What is a Leitweg-ID (Buyer Reference Route ID)? Registration, Structure & Examples

- ZUGFeRD or XRechnung: Which Format Should You Use in Germany?

- How to Validate E-Invoices in Germany: Step-by-step Guide

E-Invoicing Implementation Timeline [2025 - 2028] in Germany: Receipt, Issuance & ViDA Rollout

Germany's e-invoicing mandate rolls out in phases: Phase 1: businesses must be able to receive structured e-invoices from January 1, 2025, Phase 2: while issuance requirements for domestic B2B transactions phase in from 2027, Phase 3: with full mandatory structured invoicing from January 1, 2028. Federal B2G rules already apply separately.

The mandate covers domestic B2B transactions between German-established businesses and requires invoices in a structured electronic format that supports automated processing. EN 16931-compliant formats like XRechnung and ZUGFeRD are the standard options, with Peppol available as one transmission channel.

B2C transactions fall outside the scope, and the BMF recognizes transition-period exceptions for certain non-structured invoices during the rollout as per the BMF's official e-invoicing guidelines.

E-Invoicing Implementation Timeline & Key Deadlines in Germany

The timeline matters because Germany separates the duty to receive e-invoices from the later duty to issue them.

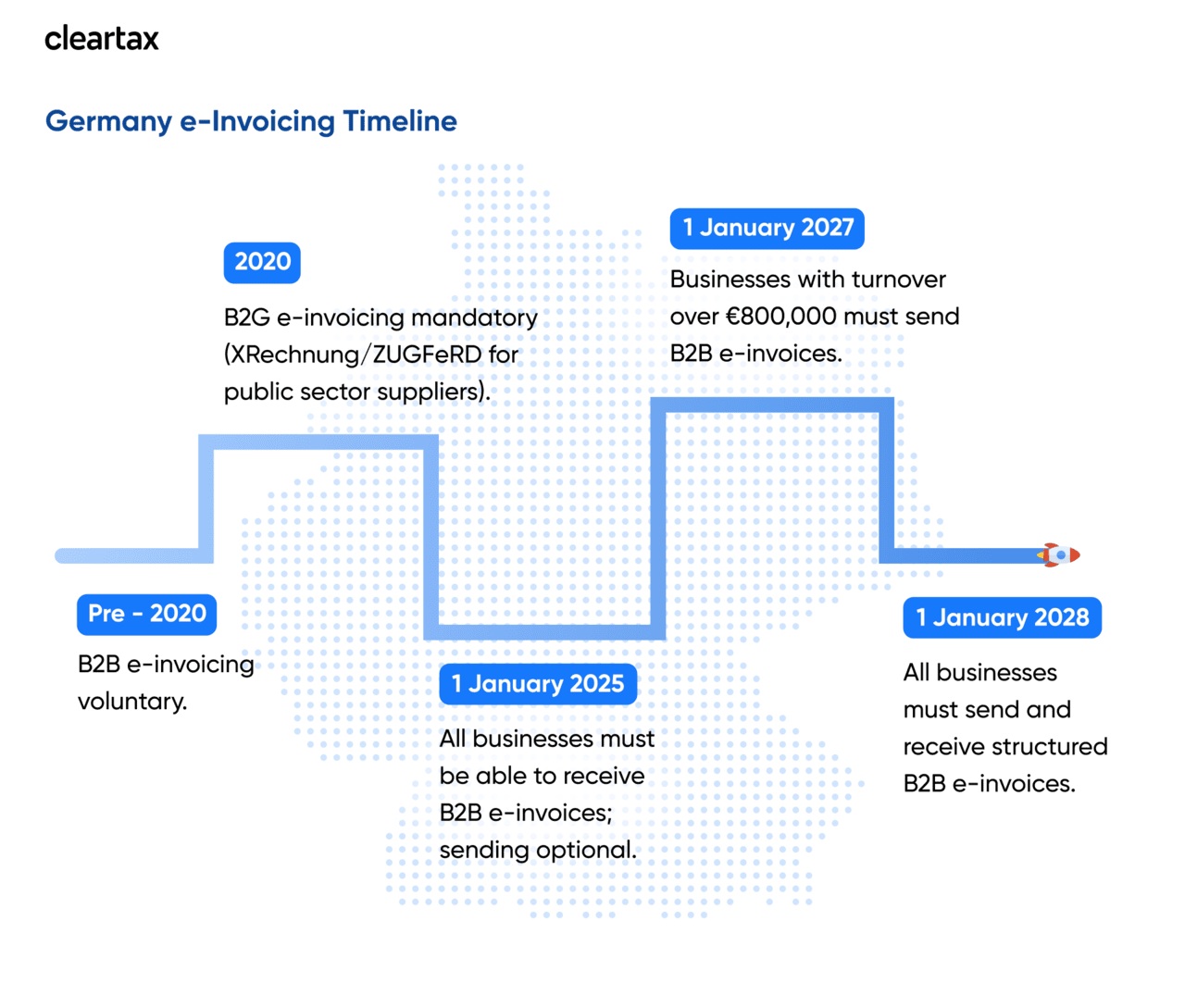

January 1, 2025: Mandatory Receipt Capability

From January 1, 2025, all businesses in scope must be able to receive e-invoices for domestic B2B transactions. This is the first operational deadline, and it applies even where a business is not yet required to issue structured invoices itself. The BMF has also clarified that businesses cannot insist on paper-first processing as the default approach once the reform takes effect.

January 1, 2025, to December 31, 2026: Broad Transition Period

The 2025 and 2026 period is the main adjustment window for issuers. During this phase, businesses may still use paper invoices, and other electronic formats such as PDFs can still be used where the recipient agrees. This gives businesses time to update ERP systems, invoice templates, validation controls, supplier and customer workflows, and archiving processes without waiting until the final deadline.

January 1, 2027: Mandatory Issuance for Larger Businesses

From 2027, the transition becomes size-based. Businesses whose prior-year turnover exceeds €800,000 must issue domestic B2B invoices as compliant e-invoices. Businesses at or below that threshold can still use the extended transition relief through the end of 2027, but they must still be able to receive e-invoices because that obligation already applied from 2025.

January 1, 2028: Broad Domestic B2B Mandate

From January 1, 2028, the broad domestic B2B transition relief ends. Businesses should assume that structured invoice generation, transmission, validation, and compliant electronic storage become part of ordinary invoicing operations. At that point, using paper or plain PDF for in-scope domestic B2B invoicing is no longer the safe compliance position.

Which Invoices Are In Scope and Which Are Not

The scope becomes easier to understand when viewed by transaction type.

- Domestic B2B invoices are the central focus of the phased mandate.

- B2C invoices are generally outside the core domestic B2B rollout.

- Federal B2G invoices follow their own public-sector framework, which has already been mandatory since 2020.

- Small invoices and certain statutory exceptions continue to matter when assessing whether a structured e-invoice is required in a particular case.

For businesses new to German e-invoicing, the practical point is simple: check transaction type first, then check the date, then check whether a transition rule or exception still applies. That approach prevents the common mistake of assuming that every invoice must follow the same rule from 2025 onward.

Timeline for B2G E-Invoicing

Germany’s B2G timeline began much earlier than its domestic B2B reform. Since November 27, 2020, suppliers to the federal administration have generally been required under the E-Invoicing Ordinance to submit electronic invoices for direct federal contracts with a net value of €1,000 or more, subject to stated exceptions.

Federal guidance now centers on OZG-RE as the federal submission portal, and businesses invoicing public bodies should always verify the exact contracting authority requirements before issuing the invoice.

How Germany’s Timeline Aligns With EU ViDA Regulations?

Germany’s domestic reform is separate from, but clearly connected to, the EU’s VAT in the Digital Age framework. The Council adopted the ViDA package on March 11, 2025, and one of its central outcomes is that VAT reporting for cross-border B2B transactions within the EU will become fully digital by 2030.

For businesses operating across multiple EU markets, Germany’s 2025 to 2028 transition should be treated as a domestic compliance project today and a preparation layer for future EU-wide digital reporting tomorrow.

Conclusion

Germany’s transition periods are not just tax dates. They are system design deadlines. Businesses that treat 2025 as only a reception rule may still reach 2027 or 2028 with weak customer data, untested invoice formats, and fragmented approval workflows. The better approach is to use the transition window as a controlled implementation phase, align legal scope with ERP reality, and make invoice exchange operational before the mandate turns process weakness into a compliance problem.

Frequently Asked Questions

About the Author

Rajan Rauniyar

I’m a Senior Content Writer at ClearTax, specializing in e-invoicing, VAT, and Tax compliance. Over the years, I’ve researched and written everything from blog posts to whitepapers and product guides, helping ClearTax expand in Malaysia, KSA, UAE, Singapore, Belgium, France and beyond. My goal is to write the most comprehensive, understandable, readable, and accurate content on any topic that has ever existed on the internet. Read more

Cleartax is a product by Defmacro Software Pvt. Ltd.

Your data security and privacy matter most to us.